LIHTC Dashboard

Local Affordability Requirements and Risks

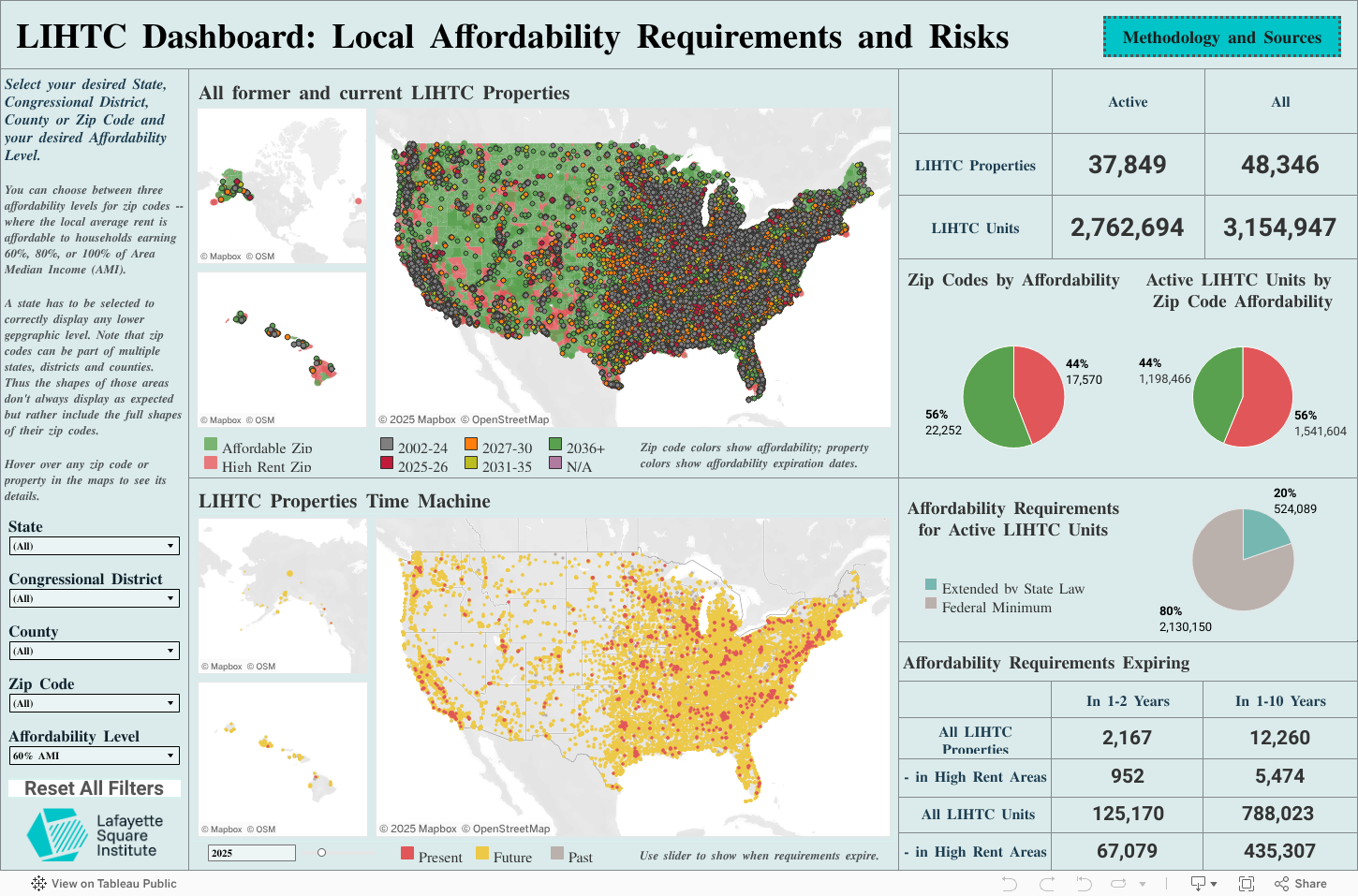

The Lafayette Square Institute data team has created the Low-Income Housing Tax Credit (LIHTC) Dashboard, an online tool that can help policymakers better understand the impact of the Low-Income Housing Tax Credit. The tool combines data from the National Housing Preservation Database (NHPD) prepared by the Public and Affordable Housing Research Corporation (PAHRC) and the National Low Income Housing Coalition (NLIHC) with data from the U.S. Census on regional rent and income characteristics.

The Dashboard maps the influence of the program and identifies properties with the highest risk of losing affordability. We have identified over 400,000 housing units at risk of losing their affordability restrictions that expire within 10 years and located in neighborhoods where the rents of those units are likely to increase and become unaffordable for lower-income families. We hope this tool can serve as a resource to local stakeholders and spur action that preserves these important affordable housing resources.

The LIHTC Dashboard:

Mapping Opportunities to Preserve Affordable Housing

Overview

Lafeyette Square Institute is a data analytics and public policy organization dedicated to aligning investors and government to help revive the American Dream. One of our core focus areas is the United States housing system and unlocking private investment to increase housing supply and affordability. We are in consistent communication with real estate investors and operators, other stakeholders in the affordable housing industry, and policymakers across the country and in Washington, D.C. Good data and data visualization is essential to ensuring all these groups can work together effectively to confront America’s housing shortage.

Our data team has created a LIHTC Dashboard, an online tool that can help practitioners and policymakers better understand the impact of the Low-Income Housing Tax Credit. This Dashboard combines multiple data sources to identify LIHTC properties at risk of losing their affordability. We plan to collaborate with public housing officials, researchers, and other industry stakeholders to use this and other data sources to highlight the importance of current programs and resources like LIHTC while also identifying new and complementary financing and public policy solutions that can increase housing supply and affordability.

Facts and Takeaways

Since its inception almost 40 years ago, the Low-Income Housing Tax Credit (LIHTC) program has served as the largest source of financing for affordable housing in the country, supporting the development or rehabilitation of over 48,000 properties, representing 3.15 million low-income units.1

- LIHTC was enacted in 1986 under the Tax Reform Act and subsidizes affordable rental housing by allocating federal tax credits to state agencies that award these credits to private developers.2 Most of the units created through the program are affordable to households earning less than 60% of the area median income (AMI) in their communities. How does AMI translate to real-world affordability? Here’s an example — to be considered affordable rent for a 3-person family earning 60% AMI in a community like Dallas, Texas ($59,580), monthly rent would need to be below $1,490s.3

As housing has become increasingly unaffordable for families across the country, the importance of programs like LIHTC is only growing.

- 50% of renter households are burdened by housing costs, spending over 30% of their income on their housing — an increase of over 10 percentage points since the year 2000.4 For lower- and moderate-income households, those primarily served by the LIHTC program, the numbers are even worse. 66% of renters earning less than 80% AMI are rent burdened, and 36% are severely rent burdened, paying over half their income on housing costs.5

While we need to explore additional ways to expand affordable housing programs, we must also ensure that currently affordable units created by programs like LIHTC are protected.

- The federal affordability requirements of LIHTC units typically last for 30 years. Those deadlines are coming up for many properties that were built in the 1990s. Some media outlets and research groups have estimated that 350,000 units could be at risk of losing their affordability by 2030, and a million by 2040.6

Lafayette Square Institute has created the LIHTC Preservation Dashboard, an interactive online tool that allows users to learn more about the LIHTC properties in their communities and identify LIHTC properties at highest risk of losing their affordability.

- The LIHTC Dashboard utilizes data from the National Housing Preservation Database on LIHTC Properties and other subsidies and the U.S. Census on regional rent and income characteristics to estimate when the affordability restrictions of LIHTC properties will expire within specific ZIP codes, counties, congressional districts and states. Following the NHPD, we assume the affordability restrictions of housing units will not expire during the extended affordability periods mandated by state policy for any type of subsidy a property receives. For example, a LIHTC property with an expired LIHTC affordability restriction will still show an active affordability restriction from a Section 8 affordability requirement. The Dashboard also provides an overlay of average rent prices at the neighborhood compared to income at the metro area level, highlighting areas where rents at a property are most likely to increase if a project’s affordability requirements expire. Users can isolate neighborhoods where average rents are affordable for families earning 60%, 80% and 100% AMI. This tool serves as a resource that highlights the importance of the LIHTC program in communities across the country while allowing policymakers and local stakeholders to identify properties with the highest risk of losing their affordability – creating opportunities to intervene and protect important affordable housing resources.

There are over 125,000 housing units with affordability restrictions that are likely to expire by the end of 2026, and nearly 800,000 units at risk of losing their affordability restrictions within 10 years.

- There are over 2,000 currently affordable properties with approximately 125,000 LIHTC units whose affordability restrictions are likely to expire by the end of 2026 and over 12,000 properties with close to 800,000 units within ten years. These numbers take both state and federal LIHTC policy into account. Per federal law, properties that received LIHTC allocations before 1990 must remain affordable for a 15-year period. For properties that received allocations after 1990, an additional 15-year restriction was added, creating a total required affordability period of 30 years. Since the program’s inception, affordability restrictions on close to 8,000 properties with over 200,000 units have expired. To avoid losing more affordable units, many states have created policies aimed at guaranteeing or encouraging project affordability that lasts beyond the federally mandated 30 years. The NHPD team has identified 14 states that have implemented additional mandatory affordability restrictions through their tax credit allocation processes. These extended requirements apply to 20% of all currently active LIHTC units.

Over half of the nearly 800,000 units with expiring affordability restrictions within the next 10 years are in high– rent areas – neighborhoods where rent increases are most likely.

- Of the around 788,000 units that have affordability restrictions that are likely to expire within 10 years, approximately 435,000 are in areas where the average rent is currently not affordable for households earning 60% of AMI. Properties are much more likely to lose their affordability in these higher-rent areas because, once a project loses its affordability restriction, the owner could raise rents to match market rents, which are unaffordable for typical LIHTC residents. By incorporating NHPD data on state policies that create extended affordability periods and highlighting high-rent communities, the Dashboard allows users to focus on a more targeted universe of properties with a higher likelihood of losing affordability. Policymakers and local stakeholders may want to prioritize identifying these units and create alternative financing and policy strategies to protect their affordability.

We need new policies and flexible financing to preserve the affordability of current LIHTC units and create more housing supply.

- According to analysis performed by Novogradac, provisions included in the recently passed reconciliation bill that extend and strengthen LIHTC could finance more than one million affordable rental homes, providing significant relief to households across the country.7 However, these additional million units still only represent a fraction of the need. According to the National Low Income Housing Coalition, there is a shortage of approximately 8.3 million units for all renters at or below 50% AMI.8

The successful example of the federal Small Business Investment Company (SBIC) program could be informative for affordable housing policy.

- For over 60 years, the SBIC program, administered by the Small Business Administration, has provided low-cost leverage to funds investing directly in small businesses.9 The program has enjoyed bipartisan support and operates at zero subsidy.10 A housing policy modeled after the SBIC could similarly provide low-cost leverage to funds – but funds that invest in affordable housing. The low-cost capital would allow funds to invest in the development of new affordable housing and the preservation of currently existing affordable housing – including LIHTC properties with expiring affordability restrictions. Because the low-cost capital provided to funds is ultimately repaid back to the government after being invested in individual properties, the program would be able to operate at zero subsidy, like the SBIC. It therefore has the potential to be scaled dramatically and create a significant volume of affordable housing.