Financing the Growth of Employee OwnershipClosing the capital gap for ESOP transitions

Employee ownership works. Yet every year, thousands of retiring owners sell to strategic buyers or private equity because the financing pathway for an ESOP transition is longer, more expensive, and less well understood than the alternatives. This paper proposes the federal and state financing tools needed to make employee ownership the default option for succession in the American middle market.

Introduction

The United States capital markets are the deepest and most liquid in the world. These features are an invaluable national asset that is responsible for the creation of trillions of dollars in private and public wealth. Despite this competitive advantage, our capital markets have not yet been meaningfully activated to maximize the wealth of American workers. To do so requires policymakers to enable the growth and scale of a proven, market-tested, and bipartisan strategy for enhancing the U.S. industrial base while building generational wealth for American workers and families—employee ownership.

The bipartisan roots and policy rationales for employee ownership first entered federal law in 1973 through the Employee Retirement Income Security Act (ERISA) championed by Senator Russell Long of Louisiana. In collaboration with attorney Louis Kelso, the enactment of the Employee Stock Ownership Plan (ESOP) structure introduced a novel legal innovation to turn American workers into owners. Fifty years later, the ESOP remains an internationally unparalleled tool in its ability to enable workers to supplement their wages with the accumulation of assets through an ownership stake in the company where they work at no cost to them.

The empirical data has consistently demonstrated that the experiment with employee ownership that began fifty years ago has been a profound success for workers, for companies, and for the broader U.S. industrial base. Employee ownership is arguably the most underrated economic policy success story in America. The topic has long flown under the radar in large part due to the fact that only a relatively small fraction of American workers have enjoyed the opportunity to become employee owners through an ESOP. An ESOP is typically formed as a product of business succession when either an owner partially or fully exits their business. While the combination of ERISA and key tax incentives have helped to produce modest levels of employee ownership in the U.S. economy,1 employee ownership remains a relatively peripheral phenomenon. Only about 2 million workers across roughly 6,000 privately held companies currently have access to significant broad-based ownership stakes—a figure that excludes public companies that are typically 1 to 5 percent ESOP-owned.2 Despite an uptick in attention in recent years and longstanding bipartisan support, employee ownership and ESOPs are frequently omitted from broader policy discussions on the topic of supporting American workers and families. This is a missed opportunity to broaden the prosperity and dynamism of American capitalism.

If employee ownership is so great, then why is it so rare? At the highest level, there are three primary impediments to the growth and scale of employee ownership and particularly the ESOP structure:

- A private financing gap

- Regulatory risk and complexity

- A lack of awareness on the part of market actors

The purpose of this white paper is to examine the nature of the private financing gap—its sources, mechanics, along with relevant policy interventions to date at the federal and state levels. The analysis will conclude with new or pending policy opportunities to mobilize private sector capital sources to create, grow, and sustain employee-owned companies. Doing so offers policymakers the chance to strengthen our industrial base by retaining the ownership of businesses operating in key productive sectors, all while building wealth and retirement security for American workers across the country.

How Do ESOPs Work?

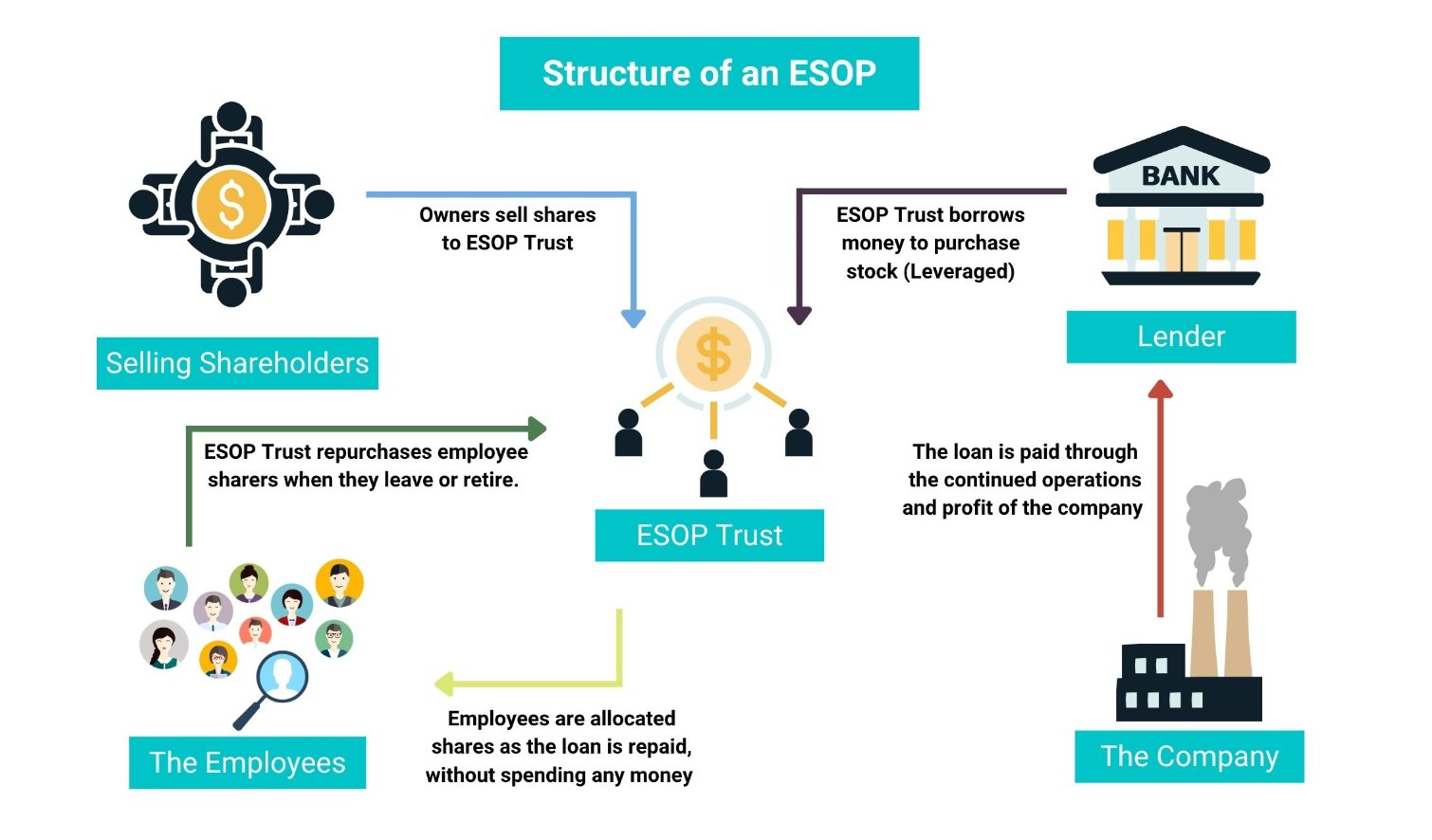

Employee ownership has a decades-long track record of creating significant social and economic value for workers, regional economies, and the financial bottom line of companies. The Employee Stock Ownership Plan (ESOP) occupies a unique place in ERISA as the only retirement benefit plan that is permitted to borrow money to finance the purchase of employer shares. In this way, the ESOP is simultaneously an employee benefit plan and corporate finance vehicle—typically enabling the buyout of a selling shareholder in the course of business succession.

Since their introduction, ESOP companies have been empirically shown to improve retention, grow faster, innovate more frequently, enjoy higher productivity, lay off fewer workers during economic downturns, and provide superior pay and benefits including an ownership stake that significantly supplements other retirement income.3 Studies have shown that employees in an ESOP company have more than double the retirement savings of non-ESOP workers. Critically, this wealth accumulation does not come at the expense of wages—additional evidence has indicated a wage premium among younger employees of ESOP companies relative to their non-ESOP peers.4 These economic benefits are exceptionally significant for low and moderate-income workers.5 Finally, employee ownership is also an effective place-based policy intervention. A sale to employees often facilitates the retention of local jobs and business investment. This is particularly valuable in low- and moderate-income areas who cannot afford to lose the mature businesses anchoring the community to a buyer that may not remain committed to local employment. Importantly, employees almost never (and should never) invest their own savings to participate in the ESOP—instead, it is an incremental benefit in addition to a diversified 401(k). Moreover, ESOP participants have the ability to partially diversify their ESOP account balance as they approach retirement age as described below.

Benefits of ESOPs

- Increased wealth and retirement security for workers

- More resilient and productive businesses

- Maintaining and building local investment

As primarily a business succession tool, most ESOP transactions are leveraged—that is, the ESOP trust borrows money from external lenders (including the selling shareholders) that is guaranteed by the company (e.g., the plan sponsor). All full-time employees are required to be eligible for the ESOP plan. As the company repays the acquisition debt through free cash flow, stock is proportionally allocated to employees through their ESOP retirement account. Typically the company stock is allocated proportionally to employees on the basis of a combination of salary and/or tenure. The stock is appraised annually, and each year the plan sponsor makes a decision to contribute to the ESOP plan as well any other retirement plans such as a 401(k) on a pre-tax basis. Vesting schedules are variable based on the design by the plan sponsor but must be no longer than six years to be fully vested. However, unlike a home mortgage there is no personal capital invested on the part of the employee (in other words, there is no down payment) and unlike a 401(k) employees do not make contributions to their plan.

When an employee leaves the company, the plan sponsor must repurchase the fully vested share value of the employee's ESOP account over a five-year period. This "repurchase obligation" requires ongoing cash flow planning on the part of the company over time. ERISA also requires ESOP participants to be able to partially diversify their accounts—e.g., convert part of their ESOP account balance into diversified, 401(k)-like portfolio—at age 55 with ten years in the plan. This feature enables partial diversification for employees in the years leading up to retirement. The ESOP structure is best suited for mature businesses with stable cash flows and diversified revenue streams. While there is no mandatory minimum size for an ESOP, generally businesses with less than 20 employees are too small. Other employee ownership structures that are a better fit for very small businesses including worker cooperatives and employee ownership trusts. ESOPs can be found in many large middle market companies6 and one of the key priorities of employee ownership finance policy is to make the structure a more consistently viable option for business owners and investors in this segment of the capital markets.

Once again, the employees do not pay out of pocket for their ESOP benefit neither at the time of the transaction nor in future company contributions—a feature that distinguishes the ESOP from its 401(k) cousin. Advocates of employee ownership do not make the argument that workers should depend only on their undiversified ESOP account with no 401(k) for their retirement security.7 A diversified 401(k)—preferably with matching, auto-enrollment, and auto-escalation—is an essential complement to the superior return upside of an ESOP. Fortunately, in practice this is not an "either/or" proposition. Most ESOP companies offer secondary diversified plans. According to the National Center for Employee Ownership (NCEO), ESOP companies are more likely to offer such a secondary plan than non-ESOP companies are to offer their employees any retirement plan at all.8

The Financing Gap

A key barrier preventing further adoption and scale of ESOPs and employee ownership is access to capital9 —specifically, the availability of attractively priced subordinated debt and equity-like capital to facilitate the sale of businesses from selling owners to their employees. Meanwhile, a record number of baby boomer business owners are now reaching retirement age and will eventually sell their company—the so-called "silver tsunami." Their most obvious options are to sell to a competitor or financial buyer that may eliminate local jobs and investment. Smaller businesses that may not have interested buyers or a family successor are at risk of closing altogether. Many owners who might prefer to preserve their legacy by selling to their employees find the option unappealing for financial and regulatory reasons.

Given that prospective employee owners generally have limited equity capital to initiate their purchase of the selling business owner's interests, transactions that would create meaningful employee ownership are often dependent upon a combination of senior debt using company assets as collateral and sellers taking back substantial subordinated, long-term notes.

The seller in these transactions must typically wait for five to ten years to fully realize the cash proceeds of the sale of their business to employees, which is often viewed as unacceptable. As a result, the overwhelming majority of ESOP transactions rely upon the relatively narrow segment of selling owners that are willing to self-finance a significant part of the transaction and wait five to ten years to fully realize their proceeds from the sale. This type of seller financing is generally considered concessionary—particularly when financial and strategic buyers routinely offer liquidity up front. As a result, the vast majority of ESOP transactions (in addition to other employee ownership structures such as employee ownership trusts and worker cooperatives) rely upon a narrow segment of selling owners that are willing and able to self-finance a significant part of the transaction and serve as a personal source of patient capital to finance the sale. This is not a financing arrangement that is well-positioned for scale, as evidenced by the stagnant growth in ESOP formation.10

How can policymakers address the seller financing problem impeding the growth of employee ownership? Progress in this area depends upon policy interventions that mobilize private institutional capital sources in order to reduce the dependence on the seller to finance a sale. Such an intervention would have the effect of lowering the opportunity cost to the business owner to sell to an ESOP and support transaction volume. It is the seller's motivation that is the fundamental determinant of whether a business will ultimately be sold to employees or another buyer. It is therefore the role of policymakers to maximize the value proposition of a sale to an ESOP, through both tax advantages and credit enhancement. This tandem of interventions along with regulatory reform would achieve the end policy objectives of American workers accumulating wealth through their ownership stake over the course of their working lives.

Simply put, the twin objectives of employee ownership finance policy are 1) to create conditions for investors to generate competitive risk-adjusted returns by deploying capital that offers liquidity to selling owners on par with non-ESOP buyers while 2) minimizing the cost of capital to the ESOP. These objectives are inherently in tension as the seller's note typically occupies the most subordinated, highest risk piece of the capital structure. Federal and state policymakers have made efforts to address the employee ownership financing gap through both existing and pending legislative initiatives. The next section of the analysis will analyze each of these initiatives in turn.

Existing Federal Financing Programs

SBA 7(A) / Main Street Employee Ownership Act of 2018

The SBA 7(a) loan guarantee program guarantees certain individual loans to small businesses by participating lenders up to 85% of principal. Banks can also sell both the guaranteed and unguaranteed portions of the individual loan into separate secondary markets, which provides the banks with the added benefit of liquidity for these loans in addition to the reduction of default risk. The maximum loan size for a 7(a) loan guarantee is $5 million, but the average loan is less than $1 million. Interest rates may be fixed or variable, generally capped at prime +2.75 percent (for loans less than $50,000, higher rates may apply). Loan terms vary according to the purpose of the loan, generally up to 25 years for real estate or 10 years for other fixed assets and working capital.

Loans guaranteed through the 7(a) program may be used for a variety of purposes including capital expenditures, working capital, and changes in ownership. In order for loans to be eligible for a 7(a) guarantee, they must meet a "credit elsewhere" test, meaning that the loan cannot be eligible under the traditional underwriting guidelines of the commercial bank. A subset of 7(a) lenders participate in the Preferred Lenders Program (PLP), which allows for streamlined approval of 7(a) loan guarantees without the involvement of SBA underwriting staff.

The Main Street Employee Ownership Act of 2018 secured a key bipartisan precedent in directing the SBA to engage in financing support of ESOPs and worker cooperatives through the 7(a) program and public outreach related to employee ownership. By enabling conversion transactions for both structures through the 7(a) program, Congress intended to provide critical financing support for the smallest businesses that otherwise would struggle to attract bank financing to facilitate a sale of a privately held business to employees via an ESOP or worker cooperative.

However, the implementation of the law to date has fallen short of Congressional objectives. Since the enactment of the legislation, SBA has reported that only seventeen ESOP transactions have been supported through the 7(a) program; the number of worker cooperative transactions is even lower.11 Several programmatic barriers hindered 7(a) loan volume for ESOP buyouts, but several of these issues have been addressed through a recent ESOP SOP released by SBA in 202312 which included the following:

- Allowed ESOP loans to be processed through the expedited Preferred Lenders Program

- Waived the traditional 10% "equity injection" requirement which was incompatible with the capital structure of ESOP transactions

- Removed the need for duplicative valuations by SBA and ERISA

Not withstanding these fixes, program implementation challenges remain. The SBA requirement that worker cooperatives must include a personal guaranty is incompatible with the nature of the structure and by passes alternative proven underwriting methods. Since nearly all worker cooperative transactions rely upon substantial seller financing, these sellers already have "skin in the game"—these seller notes are subordinate to the 7(a) guaranteed bank loan. Recent reforms by the agency provide some optimism that ESOP transaction volume will accelerate as originally intended by Congress, but challenges remain and continued monitoring will be necessary to assess ongoing progress.

State Small Business Credit Initiative (SSBCI)

In 2021, the State Small Business Credit Initiative was enacted with a $10 billion appropriation to support state-administered small business credit and investment programs. This "SSBCI 2.0" funding revived the program which had first been enacted following the 2008 financial crisis by the Obama administration at a smaller appropriation of $1.5 billion. The program is structured as an allocation to each state (usually administered by the state's development finance agency) and is eligible to be used for a range of prescribed purposes determined by the U.S. Treasury Dept. States must apply for funding through a formal application process to the Treasury Department which approves program design.

Unlike the first iteration of the program, Treasury allowed SSBCI 2.0 funds to be used by states to facilitate the sale of businesses to a majority ESOP or worker cooperative. While using program funds to purchase sellers is usually a prohibited use of funds, Treasury included a carve-out for employee ownership as an exception to this rule.13 States have discretion to allocate the funds within the broad parameters of eligibility set by Treasury. There are five types of SSBCI programs that states can adopt across two categories:14

- Capital Access Programs (CAPs): CAPs provide a portfolio loan loss reserve for which the lender and borrower contribute a share of the loan value (up to seven percent) that is matched on a dollar-for-dollar basis with SSBCI funds. Losses may be recovered from the reserve until there is no additional funding in the reserve.

- Other Credit Support Programs (OCSPs):

- Collateral support programs (CSPs): These programs provide cash to lenders to boost the value of available collateral. A collateral shortfall is a common issue in many areas experiencing economic duress.

- Loan guarantee programs (LGPs): Loan guarantees provide an assurance to lenders of partial repayment in the event a loan goes into default. Guarantees typically support businesses that do not fit standard lending criteria.

- Loan participation programs (LPPs): LPPs purchase a portion of a loan that a lender makes or make a direct loan from the state in conjunction with a private loan (companion loan). The state typically is subordinate to the lender's loan.

- Collateral support programs (CSPs): These programs provide cash to lenders to boost the value of available collateral. A collateral shortfall is a common issue in many areas experiencing economic duress.

States are required to demonstrate a "reasonable expectation" that SSBCI financing programs generate $10 of private investment or lending for every $1 in federal contributions.15

The integration of employee ownership into SSBCI 2.0 is a milestone for the field given the acknowledgment that financing the sale of businesses to employees can and should be considered a development finance priority. However, the programmatic structure of SSBCI—where funding is disbursed to states who individually must decide how to allocate the credit enhancement—is disadvantageous for employee ownership given its relative unfamiliarity as a program use case. Only Colorado's Office of Economic Development and International Trade (OEDIT) has explicitly prioritized employee ownership through its Cash Collateral Support Program as part of a broader strategy by the Governor and legislatively authorized Employee Ownership Commission.16

American Ownership and Resilience Act (AORA)

Federal policymakers are exploring new policy innovations to address the capital access challenges faced by the employee ownership field. In May 2025, the bipartisan American Ownership and Resilience Act (AORA) was introduced on a bipartisan basis in the House and Senate as a response to this impediment. Led by Senators Chris Van Hollen (D-MD), Jerry Moran (R-KS), Todd Young (R-IN), and Tammy Baldwin (D-WI) alongside Reps. Blake Moore (R-UT), Lori Trahan (D-MA), Dusty Johnson (R-SD), and Bill Foster (D-IL), the bill is designed to "crowd in" private institutional capital sources to finance scaled ESOP transactions that would simultaneously provide competitive levels of liquidity to the seller while producing market-rate risk-adjusted returns for investors. The bill would create a zero subsidy cost credit facility at the U.S. Commerce Department dedicated to providing low-cost, government-backed debt to private investment funds that are eligible to receive an Ownership Investment Company (OIC) license.

The policy design is modeled after the successful Small Business Investment Company (SBIC) program that has been administered successfully by the U.S. Small Business Administration since 1958. The SBIC program is credited with helping to jumpstart the then-nascent venture capital industry in the United States and has since operated at zero subsidy cost to the taxpayer. As with the SBIC program, Ownership Investment Companies would receive long-duration (10 year term) fixed rate debt from the Commerce Department to supplement their privately raised capital. The AORA would allow a conservative dollar-for-dollar match of low-cost leverage to privately raised capital up to a cap of $500MM. The eligible investments would be the formation, growth, and recapitalization of small and medium-sized ESOPs and worker cooperatives.

Business succession is not only a risk to local economic vitality, but it also increasingly constitutes a risk to the U.S. industrial base. Lafayette Square Institute research has found that over half of firms defined as critical by the Department of Commerce and the Department of Defense have an owner that is aged 55 or older. This means that 14% of American businesses are both in critical industries and are expected to undergo business succession in the next few years. This poses a potentially significant risk to the resilience and productive capacity of our domestic supply chains in sectors critical to economic and national security.17 Accordingly, we must recognize that ownership succession is a risk to our supply chain resilience and employee ownership as an opportunity to preserve the domestic ownership of American businesses and production over the long term.

Investment Criteria for Ownership Investment Companies

- Create: Investments that create a new majority ESOP through the voluntary sale of a private company or profitable division from an individual seller or divesting company.

- Grow: Growth capital in existing employee-owned companies that are majority employee-owned.

- Sustain: Recapitalizations of existing majority employee-owned companies that preserve the benefits of broad-based ownership for younger employees.

Mechanics of the AORA

- The legislation would create a dedicated $5B facility of low-cost leverage (debentures) that would be available exclusively for licensed Ownership Investment Companies that make eligible employee ownership investments.

- The program would operate at zero subsidy cost to the taxpayer.

- Ownership Investment Company leverage would be capped at 100% of private capital up to $500MM in order to conservatively manage program risk. In other words, larger OIC funds would only be possible to the extent that private investors are committing their own capital.

- The program would include a "bonus leverage" for investments in ESOP companies operating in industries or producing technologies deemed critical to national or economic security by the Secretary of Commerce.

- Any OIC would be required to adhere to a series of safeguard provisions to protect the interests of ESOP participants, such as prohibiting employees from providing personal financing (including the rollover of retirement plan funds) for the sale.

- Other safeguard provisions include similar ESOP best practices such as the use of independent fiduciaries and valuation advisors along with provisions that maximize value to ESOP participants in the event of a sale (event protection) and share recycling to support the longevity of the ESOP and its value for younger cohorts of employee owners.

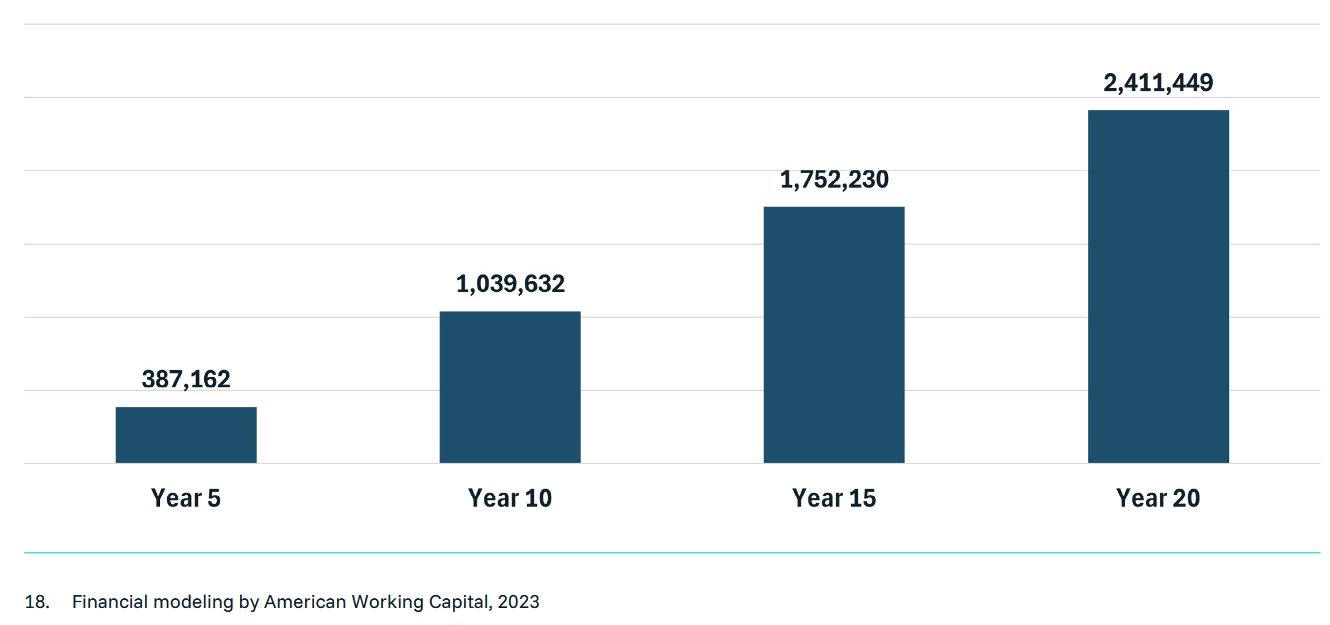

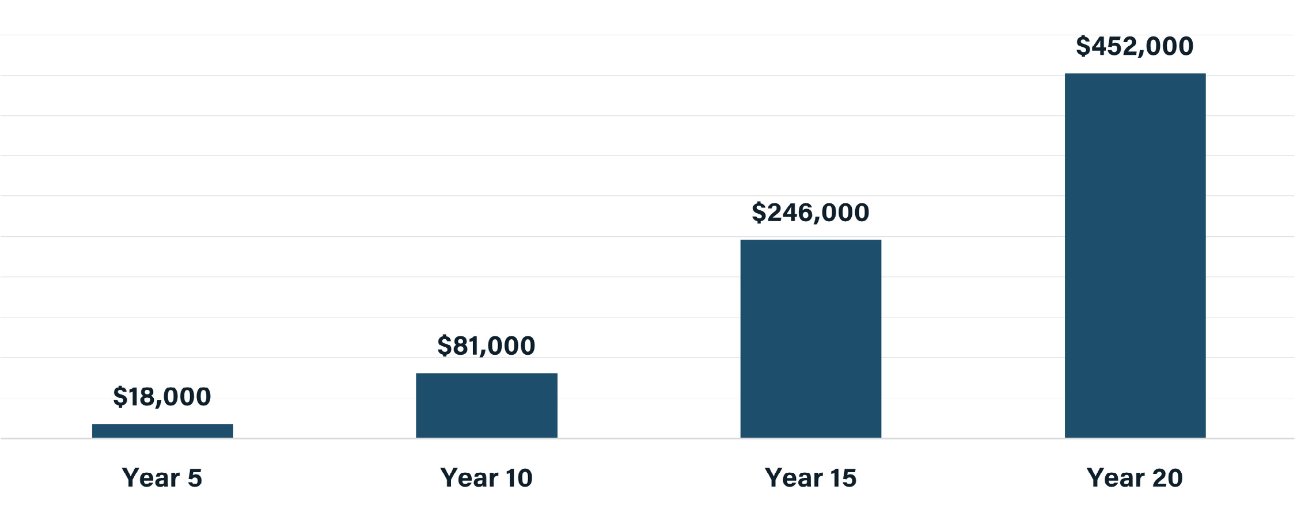

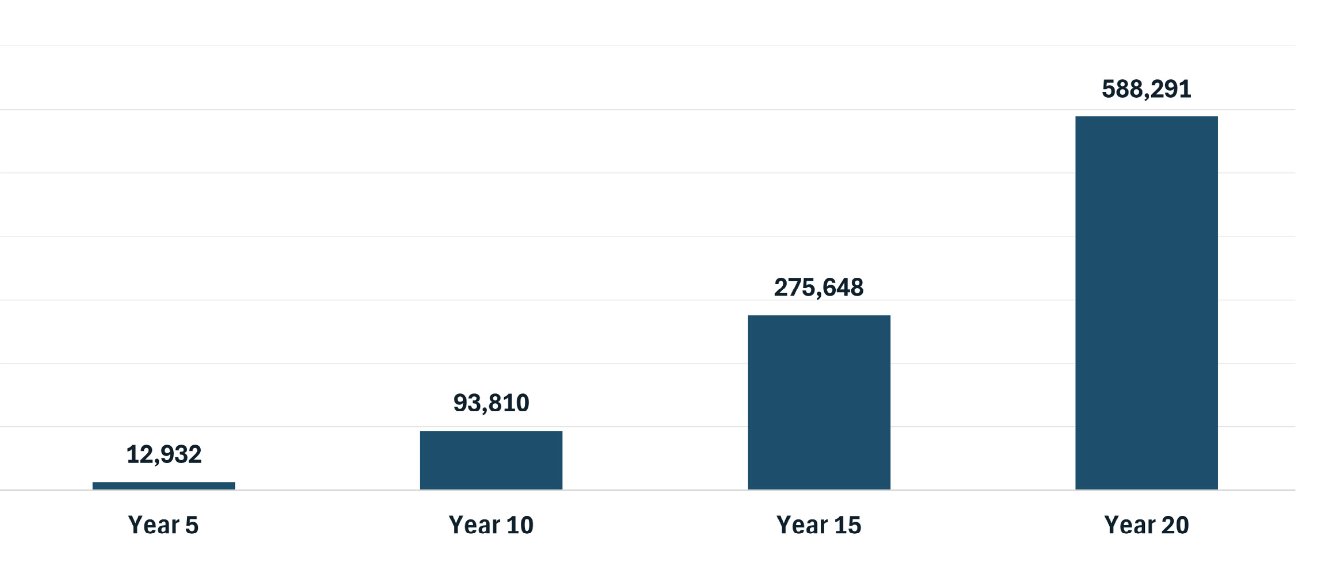

Projected Outcomes of the American Ownership & Resilience Act

According to financial modeling by American Working Capital, the AORA is projected to realize the following results over the next two decades:

State Policy Opportunities

A. State Treasurers

Policy Objective: Leverage state treasury assets to mobilize private capital to lower the overall cost of capital for an employee ownership transaction and/or reduce burden on seller notes. State Treasury assets represent a potential untapped source of financing support for employee ownership.

In Illinois, the legislature authorized the creation of the Illinois First Fund and Illinois Growth & Innovation Fund which have ringfenced 5% of state Treasury assets to capitalize a $1.5B evergreen fund to allocate to fund managers investing in Illinois infrastructure and growth capital investments, respectively. These investments are higher-yielding relative to the rest of the portfolio and do not incur fiscal costs.

Such a "carve-out" template could be applied to funds either partially or fully allocated to employee ownership strategies. By capitalizing funds with the conditionality to invest a portion of the portfolio in a given state, state Treasurers could address capital raising barriers for the niche strategy of employee ownership while in turn providing more liquidity for selling owners in that state to pursue a sale to employees. As with the Illinois examples, the higher returns would compensate for the relative illiquidity of a dedicated allocation of Treasury assets. Note that due to portfolio construction limitations, it would not be feasible to apply a requirement that all fund investments take place within the state of program operation.

This kind of investment vehicle would have the effect of "crowding in" private fund investment into the formation, growth, and/or recapitalization of in-state employee-owned businesses with a multiplier effect of mobilizing additional private capital.

B. Revolving Loan Fund

Policy Objective: Enable access to capital for the smallest businesses converting to employee ownership.

In 2023, Washington State enacted SB 5096 on a bipartisan basis which included a state revolving loan fund for ESOPs and worker cooperatives. The fund is designed to address capital access challenges by making direct loans to very small businesses in Washington State to support a sale to either employee ownership structure.

However, the state has a constitutional prohibition on providing state credit enhancement to private businesses which means the revolving loan fund needs to be federally capitalized (e.g., through the U.S. Economic Development Administration) in order to commence operations.

Most states do not have such constraints. State revolving loan funds for very small businesses who may not be able to obtain credit elsewhere could supplement the existing SSBCI toolkit with a particular focus on the smallest businesses that would struggle the most to receive bank financing. The benefit of revolving loan funds is that they are typically capitalized with a one-time appropriation that is designed to be perpetual as the proceeds from earlier loans eventually are repaid and are in turn lent out for more investments. States could also seek U.S. Economic Development Administration (EDA) funding given the federal agency's existing function of providing grant dollars to state-administered revolving loan funds for a variety of use cases.

C. Replicating SSBCI Exception at State Finance Agencies

State development finance agencies manage a wide range of loan, loan guarantee, first-loss, securitization, and other financing programs aimed at catalyzing economic growth, job creation, affordable housing supply and other priorities. These programs are typically governed by an authorizing statute and implemented with regulations promulgated by the agency.

These agencies commonly prohibit the use of program proceeds to purchase the shares of a selling business owner. Recall that the SSBCI decision to allow employee ownership investments was structured as an exception to this kind of prohibition on the use of funds by the Treasury Department. However, many state development finance agencies feature these blanket prohibitions and as a result are precluded from deploying state credit enhancement towards the conversion of in-state businesses to employee ownership.

By replicating the SSBCI exemption for the purchase of shares that result in an employee ownership structure, state development finance agencies can expand their toolkit in a way that will allow them to retain local jobs and investment while creating generational wealth for in-state residents through employee ownership.

Business Succession as Economic Development

In order for finance policy interventions at the federal and state levels to achieve maximum return on investment, state and local policymakers must have a grasp on their business ownership demographics to understand the business succession risks (and opportunities) in their jurisdictions. After all, 53% of American business owners nationally are aged 55 and above and likely to consider an exit in the next 5-10 years. While economic developers rightfully prioritize new business development and entrepreneurship, the end of the business life cycle—succession—often receives comparatively less attention. However, business succession can pose risks to the local employment and investment provided to mature businesses if the business sells to a buyer that is not committed to job creation in that area. In other words, business succession is a key retention risk for policymakers including economic developers and development finance practitioners.

In order to understand this risk, analysis and planning of the business owner demographics of a given region is a necessary first step. Project Equity has demonstrated how this could be achieved by partnering with a handful of municipalities and counties to provide analyses that quantify the business succession risk along with the economic impacts of businesses that are likely to change hands in the near future.

This kind of economic analysis and planning should be part and parcel to the toolkit along with education and outreach about business succession planning and the opportunities afforded by employee ownership structures. Such outreach is most effective when coupled with financing tools that make a sale to employees an attractive value proposition for selling business owners. The Employee Ownership Expansion Network (EOX) supports a national network of state-based outreach and technical assistance centers to accomplish exactly this purpose. Moreover, the Worker Ownership, Readiness, and Knowledge (WORK) Act passed on a bipartisan basis in 2022 that authorized $50 million of federal grant funding to bolster the capacity of state-based outreach and technical assistance on all forms of broad-based employee ownership.21 Once fully appropriated, this funding represents a significant investment in the growth of employee ownership "on the ground" infrastructure in states across the country.

However, states and municipalities are largely unaware of their business succession demographics—a critical gap in economic development planning. An opportunity exists to begin to close this knowledge and data gap by formally integrating business succession into existing economic development strategic planning currently supported by the federal government through the U.S. EDA and other agencies.

In order to qualify for many of EDA's existing funding sources, jurisdictions must formally establish an Economic Development District (EDD). According to EDA, EDDs are "multi-jurisdictional entities, commonly composed of multiple counties and in certain cases even across state borders. They help lead the locally-based, regionally driven economic development planning process that leverages the involvement of the public, private and non-profit sectors to establish a strategic blueprint (i.e. an economic development roadmap) for regional collaboration."22 One of the prerequisites for being recognized as an EDD is to publish a Economic Development Strategy (CEDS) on every five years to guide regional economic development activities. EDA offers prescriptive requirements about the content of a CEDS:

- Summary Background: A summary background of the economic conditions of the region;

- SWOT Analysis: An in-depth analysis of regional strengths, weaknesses, opportunities and threats (commonly known as a "SWOT" analysis);

- Strategic Direction/Action Plan: The strategic direction and action plan should build on findings from the SWOT analysis and incorporate/integrate elements from other regional plans (e.g., land use and transportation, workforce development, etc.) where appropriate as determined by the EDD or community/region engaged in development of the CEDS. The action plan should also identify the stakeholder(s) responsible for implementation, timetables, and opportunities for the integrated use of other local, state, and federal funds;

- Evaluation Framework: Performance measures used to evaluate the organization's implementation of the CEDS and impact on the regional economy.

The CEDS also must include a discussion of planned efforts to enhance "economic resilience" within the EDD jurisdiction. EDA defines economic resilience as "the ability of regions to anticipate, withstand, and bounce back from any type of shock, disruption, or stress that it may experience" and suggests addressing the topic either in the SWOT analysis or throughout the CEDS plan.23 The agency lists business retention and work force resiliency as examples of key economic resilience priorities.

Business succession is fundamentally a risk to local productive capacity in addition to the economic and workforce resiliency of a given region. Therefore, business succession analysis should be a standard issue component of economic development planning generally and the CEDS process in particular. This kind of analysis should either be expressly included in the set of requirements for EDDs in order to receive funding for EDA and/or otherwise incentivized with federal funding. Once appropriated, WORK Act funding should be partially allocated on the basis of a demonstrated plan to support in-state regions in investing in these kinds of analyses in tandem with employee ownership outreach and technical assistance. When it comes to retaining local businesses and maximizing the probability that a sale to employees is possible in the situations where it is appropriate, data is power for economic developers.

Conclusion

Employee ownership is an idea whose time has come. Both the empirical evidence and company experience suggest that employee ownership and ESOPs offer the chance to bolster our national competitiveness while creating generational wealth for American workers.

However, growth and scale will not be possible without solving for the financing gap that currently impedes scale. American workers do not have the capital to become meaningful shareholders on their own. A company's workers are its ultimate long-term investors with the most to gain from building long-term corporate capabilities and the most to lose from a sale to a financial or foreign buyer who is not committed to creating and retaining jobs in the United States. Through carefully tailored and fiscally conservative credit enhancement interventions at the federal and state levels, along with thoughtful economic development planning that incorporates business succession risks, policymakers at every level of government have a role to play in ensuring that American workers have the opportunity to participate in the American Dream through business ownership. Just as policymakers in the 20th century created the financing conditions for the widespread availability of home mortgages, policymakers in the 21st century have an analogous opportunity to create a stronger and more resilient U.S. industrial base while ensuring that American workers and families participate in the profound wealth creation opportunities afforded by our capital markets.

Appendix: ESOP Dashboard Terminology

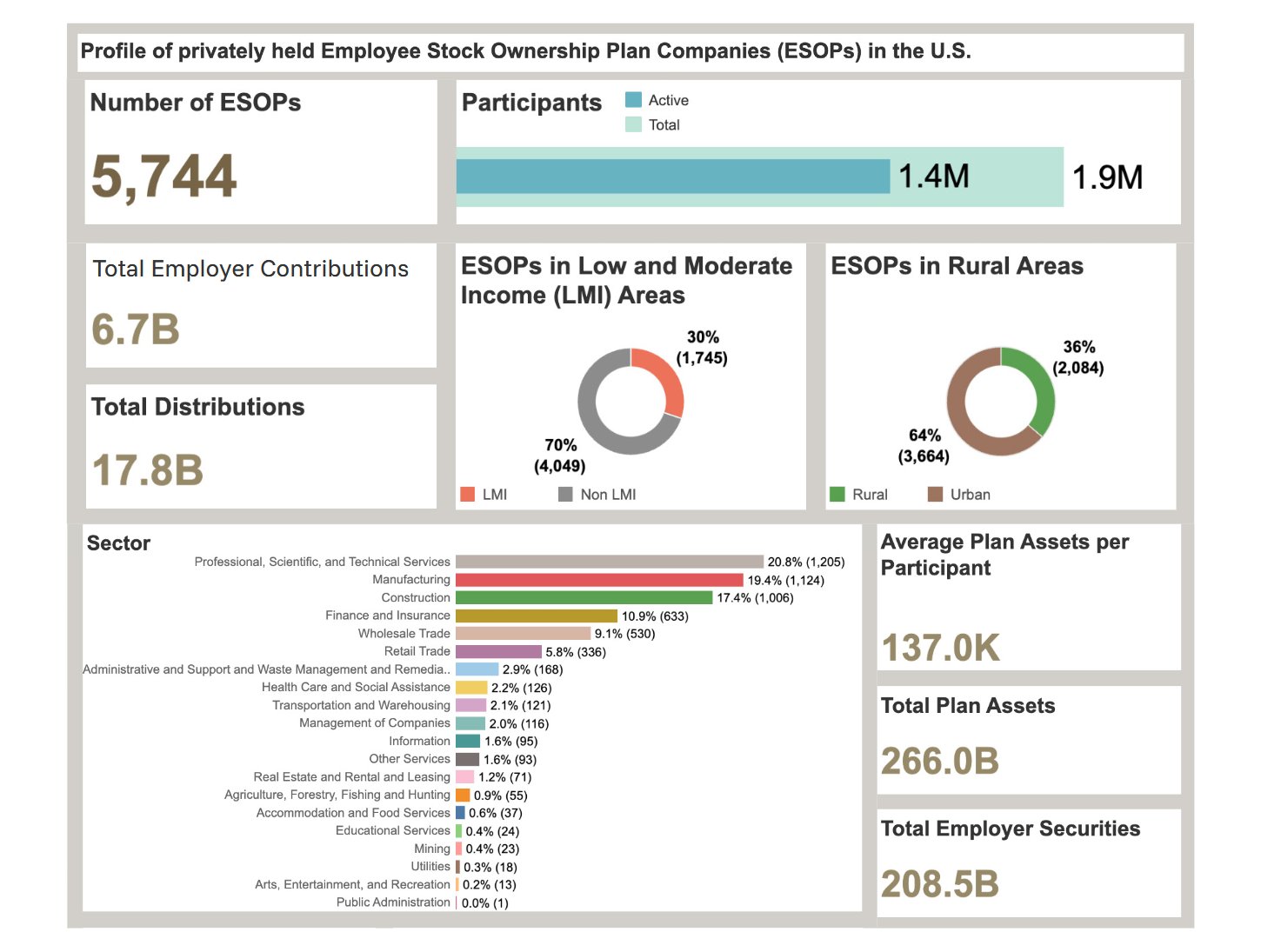

- Number of ESOPs: These are all privately held U.S. companies that are partially or fully owned by an Employee Stock Ownership Plan (ESOP). Private means they are not traded on the stock market.

- Participants: Current and former employees with ESOP account balances. Active participants are plan participants that are currently employed by the company. Total participants include active participants plus inactive participants who are no longer employed by the company but are still in the process of getting paid out by the plan.

- Total Employer Contributions: The sum total dollar amount that all privately held ESOP companies paid into their ESOP plans during the plan year.

- Total Distributions: This is how much money was paid out from ESOPs to employees or former employees in 2022. This number is substantially higher than what was paid in because many ESOPs have been in place for years. In the first few years of a new ESOP, comparatively less money is paid out (e.g., distributed to participants) because not many plan participants have exited or retired yet, so the ESOP account value accumulates over time and appreciates when the company is successful.

- Total Plan Assets: This is the dollar value of all assets in the privately held ESOPs nationally. In many cases, this value is not limited only to employer securities because tenured participants can elect to partially diversify their plan assets once they reach age 55 and 10 years in the ESOP plan.

- Total Employer Securities: This is the total dollar value of all privately held ESOPs in the U.S.

- Average Plan Assets per Participant: This is how much money the average participant in a privately held ESOP participant holds in their ESOP account.

Definitions informed by informed by the National Center for Employee Ownership (NCEO).

Lafayette Square Institute is a data analytics and public policy platform. Our mission is to bridge the gap between investors and policymakers to create economic opportunity for workers and families.

We develop, analyze, and amplify bipartisan policy solutions at the federal and state levels designed to mobilize private capital to advance the national interest. Our core areas of focus involve the intersection of private investment with employee ownership, housing supply, and access to worker benefits.

The Lafayette Square Institute team can be reached at info@lafayettesquareinstitute.org. We would be delighted to hear from you.

Contact Us.

If you are interested in learning more about the Lafayette Square Institute, please contact:

info@lafayettesquareinstitute.org